Variance Penalty In Portfolio Optimisation

Volatility is naughty

Welcome back my friends.

In case one day any of us would ever want to apply to WorldQuant, let's talk a bit more about portfolio optimisation. Better be ready than not. Today we gonna talk about a cute trick in portfolio optimisation, that is derived from first principles, very simple, comes at the cost of no extra parameter, and also has a beautiful interpretation. I'm overselling it but it is what it is your boy gotta make that bread. Let's get it.

friend sent this WorldQuant job description. ngl highkey happy to see this given that I spent the last few months just studying and writing about tree models + port opt. inshallah once I’m done w them I’m gonna start Deep Learning lets get it pic.twitter.com/vY5BnlOlFo

— quantymacro (@quantymacro) October 14, 2024

I've recommended a few students to do a project on portfolio optimisation; IMO it's a good project for quant recruitment

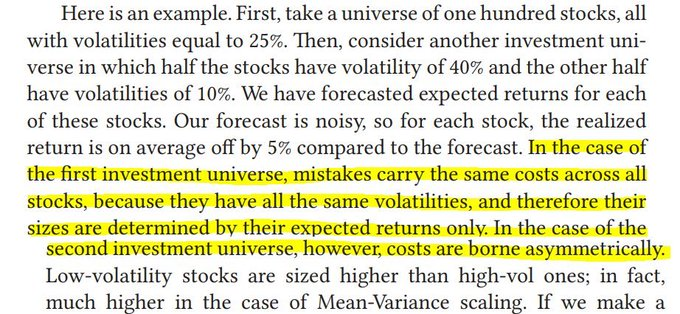

In @_paleologo's book: Advanced Portfolio Management, he wrote about an interesting experiment:

He showed that misestimation of expected returns for a low volatility asset is more detrimental than misestimation of expected returns for a high volatility asset. And we all know that vanilla MVO has a tendency to load up on low volatility assets.

Just by this observation, we will work our way into implementing a remedy to this issue. Let's dive in.